February 5, 2026

If you run a small business in Canada, insurance is probably on your mind. How much is this going to cost? Do I really need it? These are common questions, and the answers are not always simple. The cost of small business insurance in Canada depends on your business, its size, and the unique risks you face.

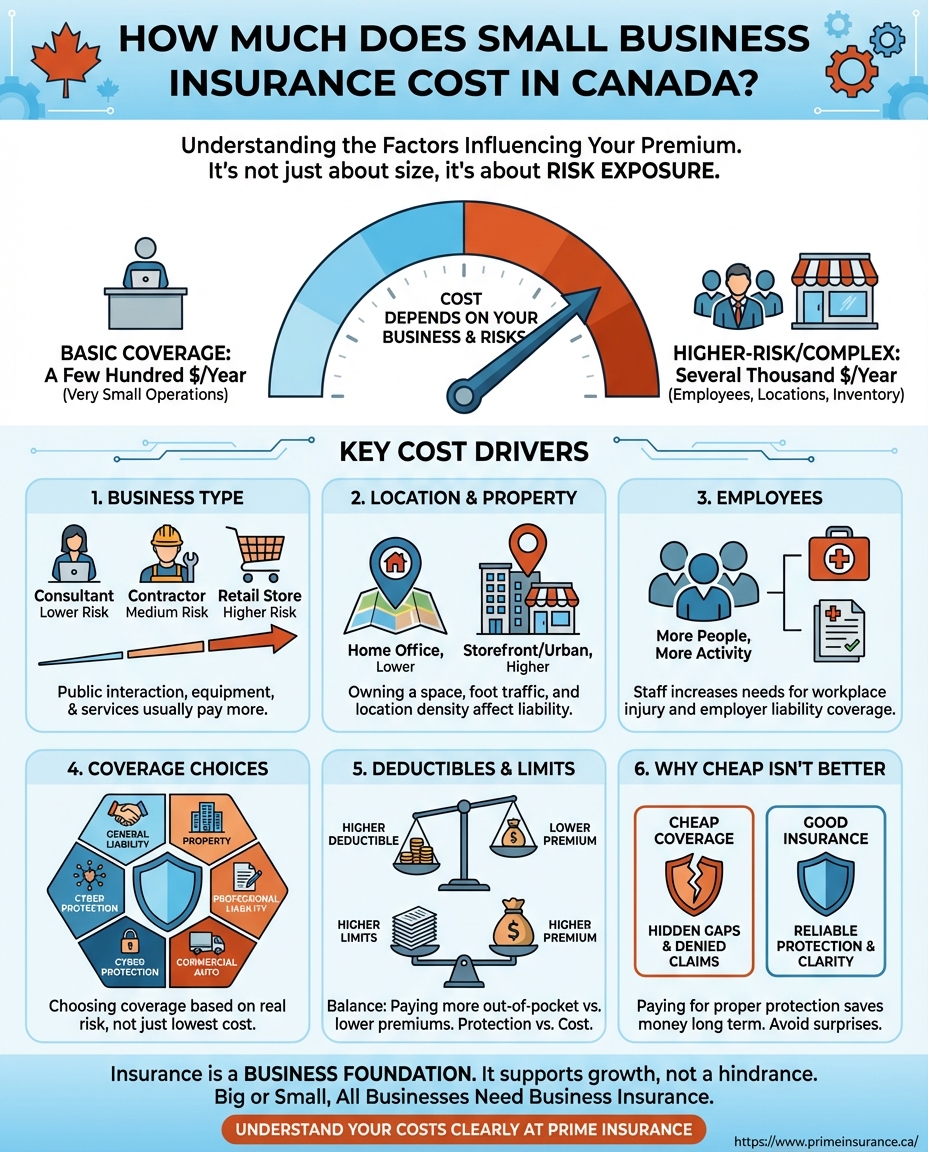

So what do most small businesses pay? In Canada, small businesses might spend anywhere from a few hundred dollars a year to several thousand. For very small operations, basic coverage generally starts at a few hundred dollars per year. For businesses with employees, physical locations, costly inventory, or higher-risk activities, costs can climb into the thousands. Insurance is not about size alone. It is about risk exposure.

This is the biggest cost driver. A home-based consultant does not face the same risks as a contractor, restaurant, or retail store. Businesses that interact with the public, handle equipment, or provide physical services usually pay more. Ask yourself this. What could realistically go wrong in a normal workday? Could someone get injured? Could the property be damaged? Could a mistake cost a client money? Insurance pricing follows these risks closely.

Where your business operates also affects cost. Renting a small office is very different from owning a storefront or warehouse. Urban areas may carry higher liability exposure simply due to foot traffic and population density. If you operate from home, your costs may be lower. If customers visit your space, insurers factor that into your premium.

Do you have staff? Even one employee changes insurance needs. Coverage such as workplace injury protection and employer liability becomes important. More people mean more activity. More activity means more potential for claims. This does not mean insurance becomes unaffordable, but it does increase the level of protection required.

Insurance is not one single product. It is a collection of protections. General liability, property coverage, professional liability, commercial auto, and cyber protection all add value in different ways. Here is the key question. What risks would hurt your business the most if they happened tomorrow? Choosing coverage based on real risk rather than cost alone keeps premiums reasonable while still protecting what matters.

If you want to lower your premium, consider choosing a higher deductible. When an accident occurs, you pay more out of pocket, but your insurance costs are reduced. Coverage limits may also affect the cost. Higher coverage means more protection but comes with higher premiums. The goal is balance. Having the right coverage to protect your business without paying for more than you need.

It is tempting to choose the lowest price and move on. But cheap coverage often leaves gaps. Those gaps only become visible when a claim is denied or limited. Good insurance should feel boring when everything is going well. It should feel reliable when something goes wrong. Paying a bit more for clarity and proper protection often saves money long term.

Think of insurance as part of your business foundation. When set up properly, it supports growth rather than holding it back. At Prime Insurance, we help Canadian small business owners understand their insurance costs clearly and confidently. We take the time to match coverage to real risks so businesses get protection that makes sense without the surprises.

You’ve poured everything into building something from the ground up, and whether you have 20 employees or 2, your business needs insurance. Business insurance helps protect against legal and financial liability in the event of accident, theft, or damage. Unfortunately,...

Get in Touch With Us

We’re open daily to help you find the right coverage or make updates to your current policy.